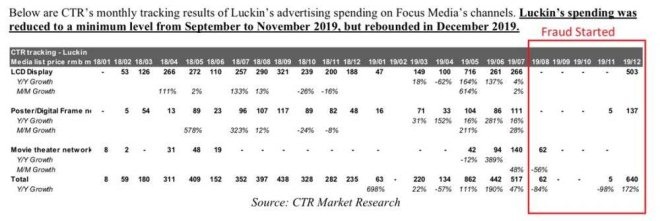

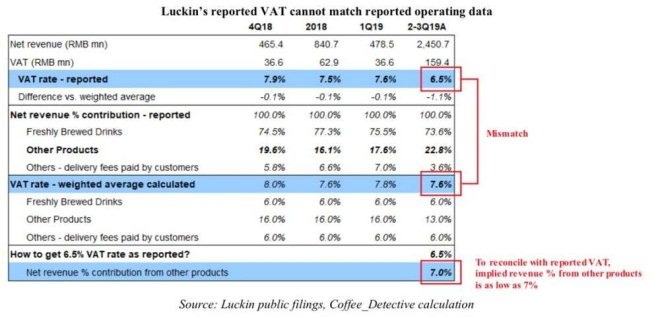

����Luckin’s revenue contribution from “other products” was only about 6% in 2019 3Q, representing a nearly 400% inflation, as shown by 25,843 customer receipts and its reported VAT numbers.

����Red Flag #1�� Luckin’s management has cashed out on 49% of their stock holdings ��or 24% of total shares outstanding�� through stock pledges, exposing investors to the risk of margin call induced price plunges

����Red Flag #2�� CAR ��699 HK��déjà vu�� Charles Zhengyao Lu and the same group of closely-connected private equity investors walked away with USD 1.6 billion from CAR ��699 HK��while minority shareholders took heavy losses

����Red Flag #3�� Through acquisition of Borgward, Luckin’s Chairman Charles Zhengyao Lu transferred RMB 137 million from UCAR ��838006 CH��to his related party, Baiyin Wang. UCAR, Borgward, and Baiyin Wang are on the hook to pay BAIC-Foton Motors RMB 5.95 billion over the next 12 months. Now Baiyin Wang owns a recently founded coffee machine vendor located next door to Luckin’s Headquarter

����Red Flag #4�� Luckin recently raised USD 865 million through a follow-on offering and a convertible bond offering to develop its “unmanned retail” strategy, which is more likely a convenient way for management to siphon large amount of cash from the company

����Red Flag #5�� Luckin’s independent board member, Sean Shao, is/was on the board of some very questionable Chinese companies listed in the US that have incurred significant losses on their public investors

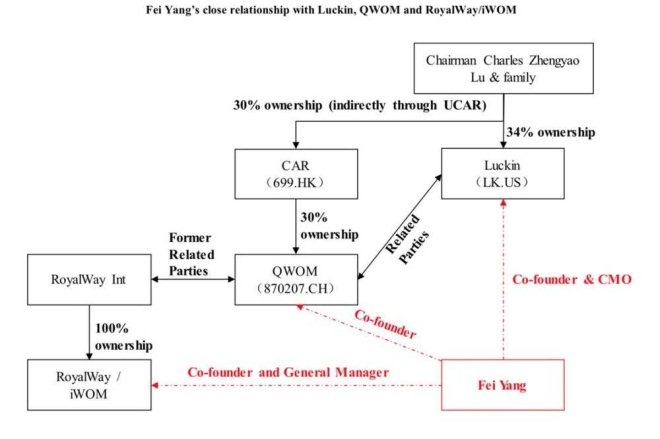

����Red Flag #6�� Luckin co-founder & Chief Marketing Officer, Fei Yang, was once sentenced to 18 months’ imprisonment for crime of illegal business operations when he was the co-founder and general manager of Beijing Koubei Interactive Marketing & Planning Co.,Ltd. ��“iWOM��. Afterwards, iWOM became a related party with Beijing QWOM Technology Co., Ltd. ��“QWOM”��, which is now an affiliate of CAR and is doing related party transactions with Luckin

����Part Two�� The Fundamentally Broken Business Before 3rd Quarter, 2019�ڶ����֣�2019���������֮ǰ����������ҵ��

����Business Model Flaw #1�� Luckin’s proposition to target core functional coffee demand is wrong�� China’s caffeine intake level of 86mg/day per capita is comparable to other Asian countries already, with 95% of the intake from tea. The market of core functional coffee product in China is small and moderately growing in China.

����Business Model Flaw #2�� Luckin’s customers are highly price sensitive and retention is driven by generous price promotion; Luckin’s attempt to decrease discount level ��i.e. raise effective price��and increase same store sales at the same time is mission impossible

����Business Model Flaw #4�� Luckin’s dream “to be part of everyone’s everyday life, starting with coffee” is unlikely to come true, as it lacks core competence in non-coffee products as well. Its “platform” is full of opportunist customers without brand loyalty. Its labor-light store model is only suitable for making “Generation 1.0” tea drinks that have been in the market for more than a decade, while leading fresh tea players have pioneered “Generation 3.0” products five years ago.

����Business Model Flaw #5�� The franchise business of Luckin Tea is subject to high compliance risk as it’s not registered with relevant authority as required by law, because Luckin Tea launched its franchise business in September 2019 without having at least two directly-operated stores fully operational for at least 1 year.